Global upstream FIDs to hit a new high in 2024 with focus on decarbonisation and deepwater resources

Mar 18, 2024

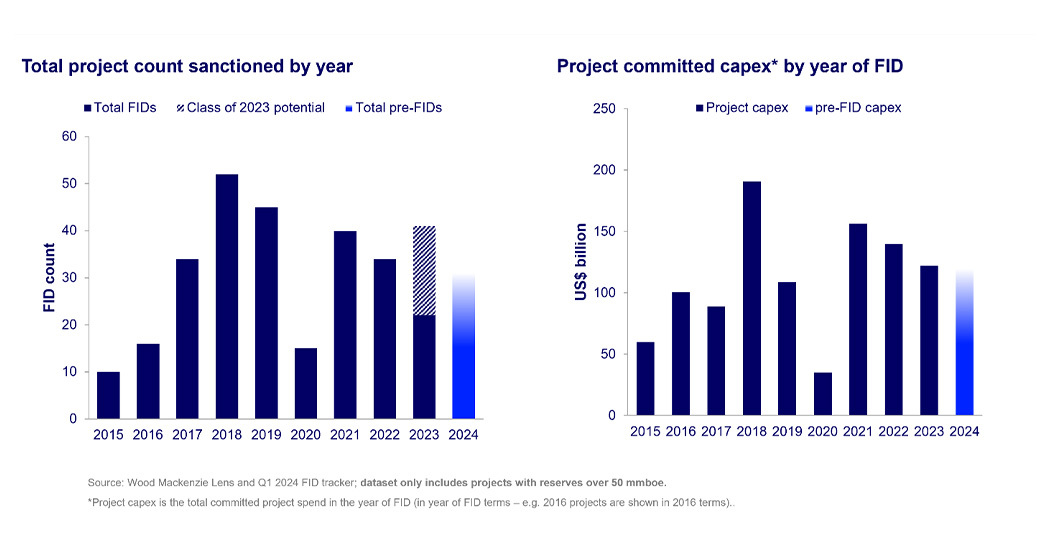

Up to 30 upstream projects larger than 50 million of barrels of oil equivalent (boe) could reach final investment decisions (FID) in 2024 for an estimated investment of US $125 billion, with the new investments putting a significant emphasis on deepwater projects and emission reduction targets, as per a new report from Wood Mackenzie.

The estimated number of upstream projects for 2024 marks an increase of nearly 27% over the 2023 numbers – which stood at 22, and comes at a time when the industry is increasingly looking at reducing emissions from upstream and midstream oil and gas activities as one of the most cost-effective ways to curb emissions by 2030.

New projects in the Middle East and LatAm

According to Wood Mackenzie’s report titled “Class of 2024: benchmarking this year’s upstream FIDs,” increased project activity in the global upstream sector this year could open up 14 boe for sanction, and total investments could touch $125 billion.

While the projected increase follows a year in which several projects were delayed or postponed, the buoyant outlook can also be attributed to a raft of new exploration and drilling opportunities in geographies such as the Middle East and Latin America.

“With many projects delayed or postponed, we expect operators to commit to more projects in 2024 than last year,” Ross McGavin, principal analyst at Wood Mackenzie, said in a statement. “National Oil Companies in the Middle East will control the most projects, but the Majors will be busy as well, particularly as they prioritise advantaged deepwater resources,” he added.

Focus on ROI and breakevens

However, generating an attractive return on investments remains a key factor in unlocking new upstream investments. As per Wood Mackenzie estimates, as the number of projects rises in 2024, breakevens for them are projected to fall, with an associated bounce back in returns (IRRs) which dipped in 2023.

The class of 2024 projects require an average of $47/bbl to generate a 15% IRR, slightly below the class of 2023’s $49/bbl, according to the global provider of data and analytics for the energy transition. The weighted average IRR for the class of 2024 is 23%, helped by a higher liquids weighting of 57% in 2024, compared to 2023’s 46% and the five-year average of 51%, the WoodMac report said.

“The higher liquids weighting and higher long-term price assumptions will improve IRRs for this year’s projects,” said McGavin. “Most payback periods are less than eight years from FID, as operators focus on rapid execution, lower unproductive capital, and higher returns.”

Alignment with OPEC’s outlook

In an exclusive interview with Energy Connects earlier this year, His Excellency Haitham Al Ghais, OPEC Secretary General, underscored 2024 as the year that will highlight the need for more investment and more projects achieving FID in the global oil industry.

“In our World Oil Outlook 2023 (WOO), over the long-term we see oil demand rising to 116 mb/d by 2045. This leads to investment requirements totaling $14 trillion, or around $610 billion on average per year. We need a long-term stable investment-friendly climate, one that works for producers and consumers and one that continues the industry’s major advances in helping reduce emissions,” HE Al Ghais told Energy Connects.

Emissions intensity below global average

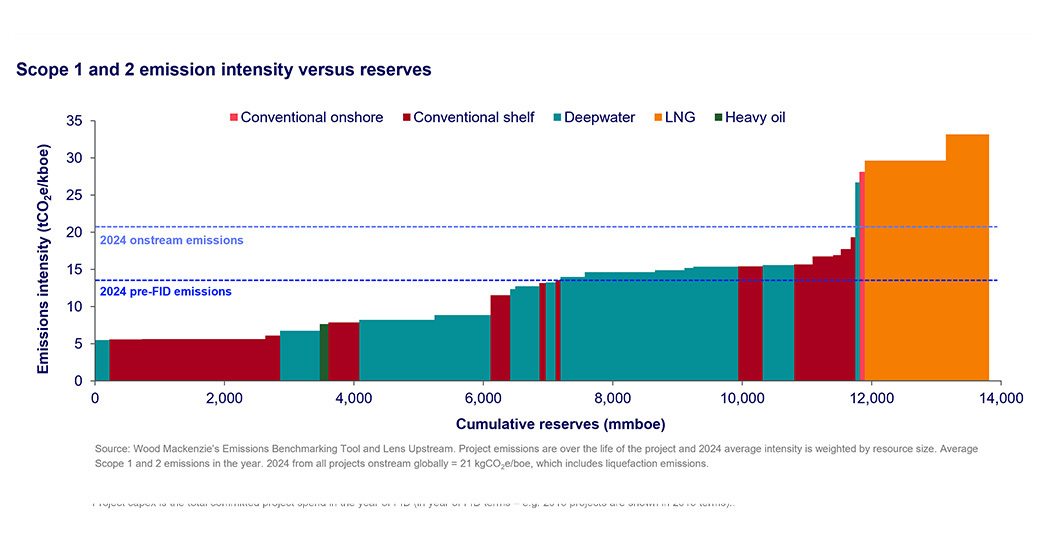

According to the Wood Mackenzie report, a majority of the upstream FIDs show a significant emphasis on deepwater projects and advantaged barrels. The average emissions intensity for the FID class of 2024 is 13.6 kgCO2e/boe, well below the global upstream average of 21 kgCO2e/boe (including liquefaction emissions), according to Wood Mackenzie’s Emissions Benchmarking tool.

“New projects are a lever to meet emission reduction goals, especially those focused on deepwater projects that continue to deliver on low emissions intensity and economic returns,” said McGavin.

According to estimates by the International Energy Agency (IEA), lowering Scope 1 and Scope 2 emissions from hydrocarbon activities is the most cost-effective way to reduce emissions by 2030 compared to any other source in the global economy, and that 15% of energy-related emissions, or 5.1 billion mt of CO2e, stem from upstream and midstream activities.

In keeping with those projections, several leading NOCs and majors have recently announced bold new pathways and investments to ensure lower-carbon operations, especially in the upstream and midstream sectors. The UAE’s ADNOC, for instance, boosted its budget for decarbonisation and lower-carbon solutions to $23 billion earlier this year and pledged to achieve near-zero methane emissions by 2030.

Related articles

Wintershall Dea proposes Stefan Schnell as new CEO following Harbour Energy transaction

Apr 25, 2024

Nearly 50% of cars sold globally to be electric by 2035 under current policy settings, says IEA

Apr 23, 2024

Europe’s energy sector at the crossroads amid push for renewables, year of elections and AI

Apr 22, 2024

S&P Global: oil and gas producers' capex cooldown won't fire up drillers' leverage

Apr 22, 2024

Namibia hosts international press conference ahead of highly anticipated Global African Hydrogen Summit 2024

Apr 22, 2024

Global wind energy industry needs policy-driven action to sustain record growth from 2023

Apr 18, 2024KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.

Top stories

Most Read

Elsewhere on Energy Connects

Chevron helping drive Egypt’s journey to become Africa’s energy powerhouse

Mar 11, 2024

Energy Workforce helps bridge the gender gap in the industry

Mar 08, 2024

EGYPES Climatech champion on a mission to combat climate change

Mar 04, 2024

Fertiglobe’s sustainability journey

Feb 29, 2024

P&O Maritime Logistics pushing for greater decarbonisation

Feb 27, 2024

India’s energy sector presents lucrative opportunities for global companies

Jan 31, 2024

Oil India charts the course to ambitious energy growth

Jan 25, 2024

Maritime sector is stepping up to the challenges of decarbonisation

Jan 08, 2024

COP28: turning transition challenges into clean energy opportunities

Dec 08, 2023

Why 2030 is a pivotal year in the race to net zero

Oct 26, 2023Partner content

Ebara Elliott Energy offers a range of products for a sustainable energy economy

Essar outlines how its CBM contribution is bolstering for India’s energy landscape

Positioning petrochemicals market in the emerging circular economy

Navigating markets and creating significant regional opportunities with Spectrum