MENA region holds strong potential for zero-carbon sources of energy

The Arab Petroleum Investments Corporation (APICORP), a multilateral development financial institution, published its MENA Power Investment Outlook 2020-2024 highlighting key regional developments and prevalent trends in the power sector over the short and medium terms.

Among the report’s key findings is the emergence of the MENA region as a strong candidate for becoming a major blue and green hydrogen-exporting region due to the combination of low-cost gas resources and low-cost renewable energy. Saudi Arabia and Morocco have already taken measurable steps to bolster their position as low-cost exporters of blue and green hydrogen, as well as net-zero ammonia and other low-carbon products.

Another key trend noted by the report is the expected uptick in planned investments directed to power transmission and distribution projects in several countries over the next five years, driven by the rise of renewables and focus on boosting regional interconnectivity.

The role of the private sector and financing in the power sector however is still largely dependent on sector reforms and government guarantees. Typically, highly leveraged power projects in the region continue to be largely financed based on non-recourse or limited recourse structure with typical debt-equity (D/E) ratios in the 60:40 to 80:20 range, or even a 85:15 D/E ratio for lower risk projects backed by strong government payment guarantees. However, regulatory reforms to support renewables and the impact of the 2020 crisis may change this balance.

Shift in power demand

The health, economic and financial fallout stemming from the COVID-19 pandemic has cost the global economy an estimated USD 1 trillion, and its impact was felt disproportionately and differently across various sectors. In the power sector, the pandemic underscored the criticality of stable electricity supplies and digital services to the economy and had a tangible effect on power demand across its three major sectors -- residential, commercial and industrial sectors. As industries and businesses reduced their operations and people spent more time at home due to lockdowns, the share of the residential sector’s electricity consumption increased at the expense of the industrial and commercial sectors.

In MENA markets, the residential sector accounts for 41 per cent of the total power demand, followed by industrial and commercial sectors at 21 per cent and 20 per cent, respectively, with the remaining 18% comprised of other sectors such as agriculture and transport, as well as network losses.

Dr. Ahmed Ali Attiga, Chief Executive Officer, APICORP, commented: “Compared to other energy sectors, the investment landscape in the power sector held relatively steady despite the COVID-19 pandemic. We expect the power sector to play a vital role in accelerating the post-pandemic recovery process as enhancing energy security and digital services take on increased strategic importance. As part of our vision to support the sustainable development of the Arab energy sector, APICORP will continue to support key projects and promising technologies that contribute to meeting these strategic regional objectives and ensure a more sustainable energy future for the region.”

Dr. Leila R. Benali, Chief Economist at APICORP, said: “Looking ahead, policy efficiency and the digitalization of the power sector weigh in as the most influential factors in the future for power demand and investments. In addition to becoming a more interconnected power market, the MENA region holds vast potential as an exporter for net-zero products, especially given the shift towards electrification from sources such as hydrogen and ammonia. This ultimately should be the vision that policymakers strive to achieve.”

Shift in power supply mix

The impact of the COVID-19 pandemic and oil price volatility led to a steady increase in the share of renewables and nuclear technologies in the power supply mix worldwide. The main accelerators for this increased penetration in the MENA region are twofold: the unprecedented cost declines in renewable energy, and governments’ renewable energy targets – which range from 13 per cent to 52 per cent of installed capacity by 2030.

However, the intermittency of renewable power sources and lack of grid-scale storage solutions means that fossil fuels – namely natural gas – and nuclear, will remain indispensable in the power supply mix in the foreseeable future. Furthermore, the penetration of renewable power in many parts of the world still largely depends on the efficacy of the relevant policies, subsidies and regulations.

Natural gas continues to be the primary energy source in the power generation mix in many MENA countries, making up more than 90 per cent of the power generation mix in Egypt, UAE and Algeria, and almost two-thirds of the power generation mix in Saudi Arabia. The rise of renewables, however, has eroded its share, falling by 2 per cent in favor of solar PV in Egypt, and by 9 per cent in favor of solar PV and the partially operational coal and nuclear powerplants in the UAE. Similarly, Morocco saw the share of oil and coal in the power generation mix fall by 2 per cent and 3 per cent, respectively, in favor of solar PV, wind and hydropower. In Jordan, natural gas saw a 5 per cent drop in favor of solar PV and wind power.

Impact of COVID-19 on investments in power projects

As noted in APICORP’s MENA Energy Investment Outlook 2020-2024 published in April, committed power sector investments held steady compared to the 2019-2023 outlook. Planned investments on the other hand decreased by around US$114 billion – a 33 per cent drop – partly due to several planned projects moving to committed status in 2020. Other factors that contributed to the decrease in planned investments were the increased surplus capacities in Egypt and Saudi Arabia, as well as stalled projects in Iran, Iraq, Tunisia and Lebanon as a direct impact of the pandemic.

Planned projects represent almost two-thirds of the total value of the current 2020-2024 MENA power sector’s project pipeline. Mirroring global trends, renewables currently own the largest share of planned and committed power projects for the period in terms of value at around one-third (32%) of total investments, followed by oil- and gas-fired power plants at nearly one-quarter (27%) of total investments, nuclear power (15%) and coal (3%).

In addition to the increased penetration of renewables, the recent push by several countries to boost regional electricity interconnectivity might lead to an increase in investments in power transmission and distribution to strengthen the grid. This includes the 3GW interconnection between Saudi Arabia and Egypt, the 2GW Euro-Africa interconnector between Egypt and Europe via Cyprus, and a 164-kilometre link between Jordan and Saudi Arabia.

Regional integration in the electricity sector in the MENA region continues to be of high strategic importance to ensure energy security. However, the COVID-19 pandemic has hindered the pace of bolstering the region’s three cross-country grids, namely North Africa, Egypt and the Levant, and the GCC.

Related articles

A Software Billionaire Is Betting Big on a Wild Climate Fix

Apr 17, 2024

European Gas Erases Year-to-Date Losses as Israel Vows Response

Apr 16, 2024

European Gas Steady as Traders See Muted Response to Iran Attack

Apr 15, 2024

Japan’s Top Power Producer Jera Considers IPO to Fund Green Push

Apr 15, 2024

MOL inaugurates central Europe’s largest green hydrogen plant

Apr 15, 2024

India Invokes Emergency Rules to Run Gas Power Plants for Summer

Apr 13, 2024KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.

More utilities news

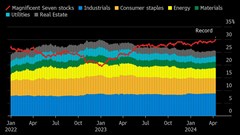

Magnificent Seven Influence Over S&P 500 Has Never Been Greater

Apr 12, 2024

China’s CGN New Energy’s Parent Said to Revive Take-Private Plan

Apr 11, 2024

Enel Hydro-Power Plant Blast in Italy Leaves at Least 3 Dead

Apr 09, 2024

Atos to Present Debt Plan as Onepoint Bolsters Rescue Coalition

Apr 08, 2024

Xcel Energy to Cut Power in Parts of Colorado Amid High Winds

Apr 06, 2024

Naturgy Said to Shelve $2.6 Billion Sale of Australia Assets

Apr 06, 2024

High Insurance Premiums Are the Latest Thing Weighing on China’s EV Market

Apr 05, 2024

Fitch Cuts Thames Water Parent to Two Steps Above Default

Apr 04, 2024

Shore-supplied power initiative will slash 1.2m tonnes of emissions from Equinor installations

Apr 04, 2024

Tesla’s Shrinking China Market Share Compounds Global Woes

Apr 03, 2024Top stories

Most Read

Elsewhere on Energy Connects

Partner content

Energy Workforce helps bridge the gender gap in the industry

Mar 08, 2024

EGYPES Climatech champion on a mission to combat climate change

Mar 04, 2024

Fertiglobe’s sustainability journey

Feb 29, 2024

Neway sees strong growth in Africa

Feb 27, 2024

P&O Maritime Logistics pushing for greater decarbonisation

Feb 27, 2024

Oil India charts the course to ambitious energy growth

Jan 25, 2024

Maritime sector is stepping up to the challenges of decarbonisation

Jan 08, 2024

COP28: turning transition challenges into clean energy opportunities

Dec 08, 2023

Why 2030 is a pivotal year in the race to net zero

Oct 26, 2023

Low carbon hydrogen holds the key to achieving net zero

Sep 29, 2023Partner content

Ebara Elliott Energy offers a range of products for a sustainable energy economy

Essar outlines how its CBM contribution is bolstering for India’s energy landscape

Positioning petrochemicals market in the emerging circular economy

Navigating markets and creating significant regional opportunities with Spectrum