Energy News

Gas & LNG

European Gas Traders Are Already Worrying About Next Winter

Apr 24, 2024

Halliburton Sees Best Profit in 12 Years Amid Smaller Shale

Apr 23, 2024

TotalEnergies agrees to purchase the remaining 50% of Malaysian upstream operator SapuraOMV

Apr 23, 2024

Heat Pump Makers Woo Contractors in Effort to Spur US Sales

Apr 22, 2024TotalEnergies launches Marsa LNG project and deploys multi-energy strategy in Oman

Apr 22, 2024

Mexico’s Sheinbaum Wants Debt-Laden Pemex to Go Green

Apr 20, 2024

Europe’s Top LNG Plant Operator Wants to Move Into Ammonia, CO2

Apr 19, 2024

Southwest Gas Unit Gets $314.8 Million From IPO, Icahn Deal

Apr 17, 2024

Kazakhstan’s Compensation Claims Against Kashagan Oil Firms Jump to $150 billion

Apr 17, 2024

Oman LNG and Shell agree 10-year supply deal amid transition-led demand growth

Apr 17, 2024Oil

Oil Holds Gain With Stockpile Data and Iran Sanctions in Focus

Apr 24, 2024

Shell, TotalEnergies in Talks for Stakes in New Adnoc LNG Plant

Apr 23, 2024

Oil Steadies Above $87 as Traders Weigh Easing Middle East Risks

Apr 23, 2024

Rolls-Royce supplies mtu gas generator sets for remote Oman oil and gas production site

Apr 23, 2024

Dirtier and Heavier Oil Is Having Its Moment as Demand Shifts

Apr 22, 2024

Oil Falls After Weekly Losses as Traders Focus on Mideast Risk

Apr 22, 2024

Skittish Oil Market Enters an Uneasy Calm Over Middle East Risk

Apr 19, 2024

Exxon’s Market Value Tops Tesla’s as Oil Rises, EV Sales Slow

Apr 19, 2024

Oil Jumps Toward $90 After Israel Is Said to Strike Iran Targets

Apr 19, 2024

AD Ports Group signs deal with ADNOC Distribution for global distribution of marine lubricants

Apr 19, 2024Renewables

US Solar Makers Seek Additional Tariffs on Panel Imports From Asia

Apr 24, 2024

Enel Forced to Raise Coupons on $11 Billion of ESG Bonds

Apr 23, 2024

SunPower Slides After Disclosing Plans to Restate Earnings

Apr 23, 2024

AFC Joins $20 Billion Morocco-to-UK Subsea Power Export Project

Apr 22, 2024

China’s Rapid Solar Growth Slows as Grid Seeks to Keep Pace

Apr 22, 2024

Europe Is Being Scorched and Flooded by Growing Climate Extremes

Apr 22, 2024

Biden Unveils Winners of $2 Billion in Green Tax Credits

Apr 19, 2024

Europe’s Demand for LNG Set to Peak in 2024 as Crisis Fades

Apr 19, 2024

Clean Hydrogen’s Best Bet May Be a Rainforest State in Borneo

Apr 18, 2024

PG&E, Edison, California Apply for $2 Billion US Grid Grant

Apr 18, 2024Technology

SLB reveals duo of innovative artificial lift systems designed to enhance performance and cut emissions

Apr 23, 2024

SLB awarded three completion contracts for Petrobras’ offshore Buzios Field

Apr 15, 2024

ACME Group and Hydrogenious LOHC Technologies to jointly explore hydrogen value chains from Oman to Europe

Apr 10, 2024

TotalEnergies to ramp up battery storage capacity in Belgium with new project

Apr 03, 2024

Borouge commits to net zero in operations by 2045

Apr 02, 2024

SLB to acquire ChampionX in all-stock transaction worth $7.75 billion

Apr 02, 2024

Eni partners with Fincantieri and RINA for maritime transport decarbonisation mission

Apr 01, 2024

SLB announces agreement to acquire majority ownership in Aker Carbon Capture

Mar 28, 2024

GE Vernova debuts AI-powered emissions management software at Ivory Coast power plant

Mar 27, 2024

FRV and Harmony Energy announce Europe’s joint largest battery storage system by MWh

Mar 22, 2024Utilities

AD Ports Group secures 20-year agreement to operate and upgrade Angolan capital’s multipurpose port terminal

Apr 25, 2024

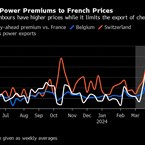

French Grid Issues Are Causing Power Prices to Soar in Europe

Apr 24, 2024

Thames Water Bond Haircut Risks Contagion, Barclays Survey Says

Apr 23, 2024

Mitsubishi Power awarded major power station upgrade contract by Kuwait to boost grid stability

Apr 23, 2024

Huayou Cuts Lithium Production, Costs on Battery Metals Rout

Apr 22, 2024

Top Czech Utility Sues Central Bank Over Fine, Aktualne Reports

Apr 20, 2024

GE Vernova reveals strategic initiatives to strengthen Iraq’s power sector

Apr 20, 2024

How a Turbine Put The Brakes on NY Offshore Wind Projects

Apr 19, 2024

CEO of Climate Group Tries to Calm Critics After Backlash

Apr 19, 2024

$1 billion deal to refurbish hydroelectric stations in Canada’s Niagara region

Apr 19, 2024Top stories

Show more latest news

Show less latest news