Features

Global wind energy industry needs policy-driven action to sustain record growth from 2023

Apr 18, 2024

Last year was the best yet for new wind energy progress as the worldwide wind industry installed a record 117GW of fresh capacity. That was the headline find of Global Wind Report 2024, released by the Global Wind Energy Council (GWEC) earlier this week.

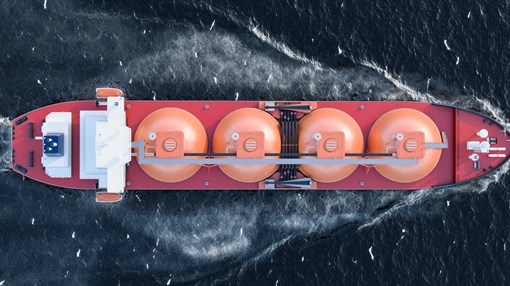

Global LNG sector maintains its grip on shipping despite growth in dual fuels

Apr 18, 2024Liquefied natural gas (LNG) remains the fuel of choice for lower-carbon shipping, despite the rise in orders for vessels equipped with dual-fuel methanol and ammonia engines, according to analysis from Rystad Energy.